| SECURITIES AND EXCHANGE COMMISSION | |

| Washington, D.C. 20549 | |

| SCHEDULE 13D | |

| Under the Securities Exchange Act of 1934 | |

|

Commvault Systems, Inc. | |

| (Name of Issuer) | |

|

Common Stock, par value $0.01 per share | |

| (Title of Class of Securities) | |

|

204166102 | |

| (CUSIP Number) | |

|

Elliott Associates, L.P. c/o Elliott Management Corporation 40 West 57th Street New York, NY 10019

with a copy to: Eleazer Klein, Esq. Schulte Roth & Zabel LLP 919 Third Avenue New York, New York 10022 (212) 756-2000 | |

| (Name, Address and Telephone Number of Person | |

| Authorized to Receive Notices and Communications) | |

|

March 21, 2018 | |

| (Date of Event Which Requires Filing of This Statement) | |

If the filing person has previously filed a statement on Schedule 13G to report the acquisition that is the subject of this Schedule 13D, and is filing this schedule because of Rule 13d-1(e), Rule 13d-1(f) or Rule 13d-1(g), check the following box. [ ]

(Page 1 of 12 Pages)

______________________________

* The remainder of this cover page shall be filled out for a reporting person's initial filing on this form with respect to the subject class of securities, and for any subsequent amendment containing information which would alter disclosures provided in a prior cover page.

The information required on the remainder of this cover page shall not be deemed to be "filed" for the purpose of Section 18 of the Securities Exchange Act of 1934 ("Act") or otherwise subject to the liabilities of that section of the Act but shall be subject to all other provisions of the Act (however, see the Notes).

| CUSIP No. 204166102 | Schedule 13D | Page 2 of 12 Pages |

| 1 |

NAME OF REPORTING PERSON Elliott Associates, L.P. | |||

| 2 | CHECK THE APPROPRIATE BOX IF A MEMBER OF A GROUP |

(a) x (b) ¨ | ||

| 3 | SEC USE ONLY | |||

| 4 |

SOURCE OF FUNDS WC | |||

| 5 | CHECK BOX IF DISCLOSURE OF LEGAL PROCEEDING IS REQUIRED PURSUANT TO ITEMS 2(d) or 2(e) | ¨ | ||

| 6 |

CITIZENSHIP OR PLACE OF ORGANIZATION Delaware | |||

| NUMBER OF SHARES BENEFICIALLY OWNED BY EACH REPORTING PERSON WITH: |

7 |

SOLE VOTING POWER 1,067,706 (1) | ||

| 8 |

SHARED VOTING POWER -0- | |||

| 9 |

SOLE DISPOSITIVE POWER 1,067,706 (1) | |||

| 10 |

SHARED DISPOSITIVE POWER -0- | |||

| 11 |

AGGREGATE AMOUNT BENEFICIALLY OWNED BY EACH PERSON 1,067,706 (1) | |||

| 12 | CHECK IF THE AGGREGATE AMOUNT IN ROW (11) EXCLUDES CERTAIN SHARES | ¨ | ||

| 13 |

PERCENT OF CLASS REPRESENTED BY AMOUNT IN ROW (11) 2.4% | |||

| 14 |

TYPE OF REPORTING PERSON PN | |||

(1) Includes 395,707 shares of Common Stock underlying Physical Derivative Agreements.

| CUSIP No. 204166102 | Schedule 13D | Page 3 of 12 Pages |

| 1 |

NAME OF REPORTING PERSON Elliott International, L.P. | |||

| 2 | CHECK THE APPROPRIATE BOX IF A MEMBER OF A GROUP |

(a) x (b) ¨ | ||

| 3 | SEC USE ONLY | |||

| 4 |

SOURCE OF FUNDS WC | |||

| 5 | CHECK BOX IF DISCLOSURE OF LEGAL PROCEEDING IS REQUIRED PURSUANT TO ITEMS 2(d) or 2(e) | ¨ | ||

| 6 |

CITIZENSHIP OR PLACE OF ORGANIZATION Cayman Islands, British West Indies | |||

| NUMBER OF SHARES BENEFICIALLY OWNED BY EACH REPORTING PERSON WITH: |

7 |

SOLE VOTING POWER -0- | ||

| 8 |

SHARED VOTING POWER 2,268,878 (1) | |||

| 9 |

SOLE DISPOSITIVE POWER -0- | |||

| 10 |

SHARED DISPOSITIVE POWER 2,268,878 (1) | |||

| 11 |

AGGREGATE AMOUNT BENEFICIALLY OWNED BY EACH PERSON 2,268,878 (1) | |||

| 12 | CHECK IF THE AGGREGATE AMOUNT IN ROW (11) EXCLUDES CERTAIN SHARES | ¨ | ||

| 13 |

PERCENT OF CLASS REPRESENTED BY AMOUNT IN ROW (11) 5.0% | |||

| 14 |

TYPE OF REPORTING PERSON PN | |||

(1) Includes 840,877 shares of Common Stock underlying Physical Derivative Agreements.

| CUSIP No. 204166102 | Schedule 13D | Page 4 of 12 Pages |

| 1 |

NAME OF REPORTING PERSON Elliott International Capital Advisors Inc. | |||

| 2 | CHECK THE APPROPRIATE BOX IF A MEMBER OF A GROUP | (a) x (b) ¨ | ||

| 3 | SEC USE ONLY | |||

| 4 |

SOURCE OF FUNDS OO | |||

| 5 | CHECK BOX IF DISCLOSURE OF LEGAL PROCEEDING IS REQUIRED PURSUANT TO ITEMS 2(d) or 2(e) | ¨ | ||

| 6 |

CITIZENSHIP OR PLACE OF ORGANIZATION Delaware | |||

| NUMBER OF SHARES BENEFICIALLY OWNED BY EACH REPORTING PERSON WITH: |

7 |

SOLE VOTING POWER -0- | ||

| 8 |

SHARED VOTING POWER 2,268,878 (1) | |||

| 9 |

SOLE DISPOSITIVE POWER -0- | |||

| 10 |

SHARED DISPOSITIVE POWER 2,268,878 (1) | |||

| 11 |

AGGREGATE AMOUNT BENEFICIALLY OWNED BY EACH PERSON 2,268,878 (1) | |||

| 12 | CHECK IF THE AGGREGATE AMOUNT IN ROW (11) EXCLUDES CERTAIN SHARES | ¨ | ||

| 13 |

PERCENT OF CLASS REPRESENTED BY AMOUNT IN ROW (11) 5.0% | |||

| 14 |

TYPE OF REPORTING PERSON CO | |||

(1) Includes 840,877 shares of Common Stock underlying Physical Derivative Agreements.

| CUSIP No. 204166102 | Schedule 13D | Page 5 of 12 Pages |

| Item 1. | SECURITY AND ISSUER |

| This statement relates to the shares of common stock, par value $0.01 per share (the "Common Stock"), of Commvault Systems, Inc., a Delaware corporation (the "Issuer"). The Issuer's principal executive offices are located at 1 Commvault Way, Tinton Falls, New Jersey 07724. | |

| Item 2. | IDENTITY AND BACKGROUND |

| (a)-(c) This statement is being filed by Elliott Associates, L.P., a Delaware limited partnership, and its wholly-owned subsidiaries (collectively, "Elliott" or "we"), Elliott International, L.P., a Cayman Islands limited partnership ("Elliott International"), and Elliott International Capital Advisors Inc., a Delaware corporation ("EICA" and collectively with Elliott and Elliott International, the "Reporting Persons"). Elliott Advisors GP LLC, a Delaware limited liability company ("Elliott Advisors"), which is controlled by Paul E. Singer ("Singer"), Elliott Capital Advisors, L.P., a Delaware limited partnership ("Capital Advisors"), which is controlled by Singer, and Elliott Special GP, LLC, a Delaware limited liability company ("Special GP"), which is controlled by Singer, are the general partners of Elliott. Hambledon, Inc., a Cayman Islands corporation ("Hambledon"), which is also controlled by Singer, is the sole general partner of Elliott International. EICA is the investment manager for Elliott International. EICA expressly disclaims equitable ownership of and pecuniary interest in any shares of Common Stock. |

|

ELLIOTT The business address of Elliott is 40 West 57th Street, New York, New York 10019. The principal business of Elliott is to purchase, sell, trade and invest in securities. |

|

SINGER Singer's business address is 40 West 57th Street, New York, New York 10019. Singer's principal business is to serve as the sole managing member of Elliott Advisors, as a general partner of Capital Advisors, as the president of EICA, and as a managing member of Special GP. |

|

CAPITAL ADVISORS The business address of Capital Advisors is 40 West 57th Street, New York, New York 10019. The principal business of Capital Advisors is the furnishing of investment advisory services. Capital Advisors also serves as a managing member of Special GP and as a general partner of Elliott. The names, business addresses, and present principal occupation or employment of the general partners of Capital Advisors are as follows: |

| NAME | ADDRESS | OCCUPATION |

| Paul E. Singer |

40 West 57th St. New York, New York 10019 |

Sole Managing Member of Elliott Advisors; General partner of Capital Advisors; President of EICA; and a managing member of Special GP |

| Braxton Associates, Inc. |

40 West 57th St. New York, New York 10019 |

The principal business of Braxton Associates, Inc. is serving as general partner of Capital Advisors |

| CUSIP No. 204166102 | Schedule 13D | Page 6 of 12 Pages |

| Elliott Asset Management LLC |

40 West 57th St. New York, New York 10019 |

General Partner of Capital Advisors |

| The name, business address, and present principal occupation or employment of the sole director and executive officer of Braxton Associates, Inc. are as follows: |

| NAME | ADDRESS | OCCUPATION |

| Paul E. Singer |

40 West 57th St. New York, New York 10019 |

Sole Managing Member of Elliott Advisors; General partner of Capital Advisors; President of EICA; and a managing member of Special GP |

|

ELLIOTT SPECIAL GP, LLC The business address of Special GP is 40 West 57th Street, New York, New York 10019. The principal business of Special GP is serving as a general partner of Elliott. The names, business address, and present principal occupation or employment of the managing members of Special GP are as follows: |

| NAME | ADDRESS | OCCUPATION |

| Paul E. Singer |

40 West 57th St. New York, New York 10019 |

Sole Managing Member of Elliott Advisors; General partner of Capital Advisors; President of EICA; and a managing member of Special GP |

| Braxton Associates, Inc. |

40 West 57th St. New York, New York 10019 |

The principal business of Braxton Associates, Inc. is serving as general partner of Capital Advisors |

| Elliott Asset Management LLC |

40 West 57th St. New York, New York 10019 |

General Partner of Capital Advisors |

|

ELLIOTT ADVISORS The business address of Elliott Advisors is 40 West 57th Street, New York, New York 10019. The principal business of Elliott Advisors is serving as a general partner of Elliott. The name, business address, and present principal occupation or employment of the sole managing member of Elliott Advisors are as follows: |

| NAME | ADDRESS | OCCUPATION |

| Paul E. Singer |

40 West 57th St. New York, New York 10019 |

Sole Managing Member of Elliott Advisors; General partner of Capital Advisors; President of EICA; and a managing member of Special GP |

| CUSIP No. 204166102 | Schedule 13D | Page 7 of 12 Pages |

|

ELLIOTT INTERNATIONAL The business address of Elliott International is c/o Maples & Calder, P.O. Box 309, Ugland House, South Church Street, George Town, Cayman Islands, British West Indies. The principal business of Elliott International is to purchase, sell, trade and invest in securities. The name, business address, and present principal occupation or employment of the general partner of Elliott International is as follows: |

| NAME | ADDRESS | OCCUPATION |

| Hambledon, Inc. |

c/o Maples & Calder P.O. Box 309 Ugland House South Church Street George Town, Cayman Islands British West Indies |

General partner of Elliott International |

|

HAMBLEDON The name, business address, and present principal occupation or employment of the sole director and executive officer of Hambledon are as follows: |

| NAME | ADDRESS | OCCUPATION |

| Paul E. Singer |

40 West 57th St. New York, New York 10019 |

Sole Managing Member of Elliott Advisors; General partner of Capital Advisors; President of EICA; and a managing member of Special GP |

|

EICA The business address of EICA is 40 West 57th Street New York, New York 10019. The principal business of EICA is to act as investment manager for Elliott International. The name, business address, and present principal occupation or employment of the sole director and executive officer of EICA is as follows: |

| NAME | ADDRESS | OCCUPATION |

| Paul E. Singer |

40 West 57th St. New York, New York 10019 |

Sole Managing Member of Elliott Advisors; General partner of Capital Advisors; President of EICA; and a managing member of Special GP |

| (d) and (e) During the last five years, none of the persons or entities listed above has been (i) convicted in a criminal proceeding (excluding traffic violations or similar misdemeanors); or (ii) a party to a civil proceeding of a judicial or administrative body of competent jurisdiction and as a result of such proceeding was or is subject to a judgment, decree or final order enjoining future violations of, or prohibiting or mandating activities subject to, federal or state securities laws or finding any violation with respect to such laws. |

| (f) Singer is a citizen of the United States of America. |

| CUSIP No. 204166102 | Schedule 13D | Page 8 of 12 Pages |

| Item 3. | SOURCE AND AMOUNT OF FUNDS OR OTHER CONSIDERATION |

|

Elliott Working Capital

|

The aggregate purchase price of the shares of Common Stock directly owned by Elliott is approximately $36,082,896. The aggregate purchase price of the Physical Derivative Agreements owned by Elliott is approximately $22,743,350. |

| Elliott International Working Capital | The aggregate purchase price of the shares of Common Stock directly owned by Elliott International is approximately $76,676,325. The aggregate purchase price of Physical Derivative Agreements owned by Elliott International is approximately $48,329,597. |

| The Reporting Persons may effect purchases of the shares of Common Stock through margin accounts maintained for them with prime brokers, which extend margin credit as and when required to open or carry positions in their margin accounts, subject to applicable federal margin regulations, stock exchange rules and such firms' credit policies. Positions in the shares of Common Stock may be held in margin accounts and may be pledged as collateral security for the repayment of debit balances in such accounts. Since other securities may be held in such margin accounts, it may not be possible to determine the amounts, if any, of margin used to purchase the shares of Common Stock. |

| Item 4. | PURPOSE OF TRANSACTION |

| The Reporting Persons believe the securities of the Issuer are undervalued and represent an attractive investment opportunity. The Reporting Persons believe that the Issuer requires fundamental changes throughout its business and that the Issuer can significantly improve shareholder value through operational initiatives, capital allocation changes and enhanced management and Board of Directors (the "Board") leadership. On April 2, 2018, the Reporting Persons sent a letter to the Issuer's Board, which is attached hereto as Exhibit 99.2, detailing their views on improving the Issuer's performance and increasing shareholder value. Additionally, on April 2, 2018, the Reporting Persons delivered a nomination letter to the Issuer nominating Martha Bejar, Wendy Lane, John McCormack and Chuck Moran for election to the Board at the Issuer's 2018 annual meeting of shareholders. |

| The Reporting Persons intend to consider, explore and/or develop plans and/or make proposals with respect to, among other things, the matters set forth in the previous paragraph (including the matters set forth in Exhibit 99.2) and potential changes in, the Issuer's operations, management, organizational documents, Board composition, ownership, capital or corporate structure, sale transactions, dividend policy, and strategy and plans. The Reporting Persons intend to communicate with the Issuer's management and Board about, and may enter into negotiations with them regarding, the foregoing and a broad range of operational and strategic matters and to communicate with other shareholders or third parties, including potential acquirers, service providers and financing sources regarding the Issuer. The Reporting Persons may exchange information with any such persons pursuant to appropriate confidentiality or similar agreements. The Reporting Persons may change their intentions with respect to any and all matters referred to in this item 4. They may also take steps to explore and prepare for various plans and actions, and propose transactions, before forming an intention to engage in such plans or actions or proceed with such transactions. |

| CUSIP No. 204166102 | Schedule 13D | Page 9 of 12 Pages |

| The Reporting Persons intend to review their investment in the Issuer on a continuing basis and depending upon various factors, including without limitation, the Issuer's financial position and strategic direction, the outcome of any discussions referenced above, overall market conditions, other investment opportunities available to the Reporting Persons, and the availability of securities of the Issuer at prices that would make the purchase or sale of such securities desirable, the Reporting Persons may endeavor (i) to increase or decrease their respective positions in the Issuer through, among other things, the purchase or sale of securities of the Issuer, including through transactions involving the shares of Common Stock and/or other equity, debt, notes, other securities, or derivative or other instruments that are based upon or relate to the value of securities of the Issuer in the open market or in private transactions, including through a trading plan created under Rule 10b5-1(c) or otherwise, on such terms and at such times as the Reporting Persons may deem advisable and/or (ii) to enter into transactions that increase or hedge their economic exposure to the Common Stock without affecting their beneficial ownership of shares of Common Stock. In addition, the Reporting Persons may, at any time and from time to time, (i) review or reconsider their position and/or change their purpose and/or formulate plans or proposals with respect thereto and (ii) consider or propose one or more of the actions described in subparagraphs (a) - (j) of Item 4 of Schedule 13D. |

| Item 5. | INTEREST IN SECURITIES OF THE ISSUER |

|

(a) As of the date hereof, Elliott, Elliott International and EICA collectively have beneficial ownership of 3,336,584 shares of Common Stock constituting approximately 7.4% of the shares of Common Stock outstanding and combined economic exposure in the Issuer equivalent to 4,618,310 shares of Common Stock constituting approximately 10.3% of the shares of Common Stock outstanding.

|

|

The aggregate percentage of the Common Stock reported owned by each person named herein is based upon 44,942,269 shares of Common Stock outstanding, which is the total number of shares of Common Stock outstanding as of January 22, 2018 as reported in the Issuer's Quarterly Report on Form 10-Q for the quarterly period ended December 31, 2017, filed with the Securities and Exchange Commission (the "SEC") on January 25, 2018.

|

|

As of the date hereof, Elliott beneficially owned 1,067,706 shares of Common Stock, including 395,707 shares of Common Stock underlying Physical Derivative Agreements that Elliott may be deemed to beneficially own upon satisfaction of certain conditions, constituting 2.4% of the shares of Common Stock outstanding.

|

| As of the date hereof, Elliott International beneficially owned 2,268,878 shares of Common Stock, including 840,877 shares of Common Stock underlying Physical Derivative Agreements that Elliott International may be deemed to beneficially own upon satisfaction of certain conditions, constituting 5.0% of the shares of Common Stock outstanding. EICA, as the investment manager of Elliott International may be deemed to beneficially own the 2,268,878 shares of Common Stock beneficially owned by Elliott International, constituting 5.0% of the shares of Common Stock outstanding. |

|

(b) Elliott has the power to vote or direct the vote of, and to dispose or direct the disposition of the shares of Common Stock owned directly by it.

|

| CUSIP No. 204166102 | Schedule 13D | Page 10 of 12 Pages |

|

Elliott International has the shared power with EICA to vote or direct the vote of, and to dispose or direct the disposition of, the shares of Common Stock owned directly by Elliott International. Information regarding each of Elliott International and EICA is set forth in Item 2 of this Schedule 13D and is expressly incorporated by reference herein.

|

| (c) The transactions effected by the Reporting Persons during the past 60 days are set forth on Schedule 1 attached hereto. |

|

(d) No person other than Elliott has the right to receive or the power to direct the receipt of dividends from, or the proceeds from the sale of, the shares of Common Stock beneficially owned by Elliott.

No person other than Elliott International and EICA has the right to receive or the power to direct the receipt of dividends from, or the proceeds from the sale of, the shares of Common Stock beneficially owned by Elliott International and EICA. |

| (e) Not applicable. |

| Item 6. | CONTRACTS, ARRANGEMENTS, UNDERSTANDINGS OR RELATIONSHIPS WITH RESPECT TO SECURITIES OF THE ISSUER |

|

Elliott and Elliott International have entered into notional principal amount derivative agreements in the form of physically settled swaps (the "Physical Derivative Agreements") with respect to 395,707 and 840,877 shares of Common Stock of the Issuer, respectively, that the Reporting Persons may be deemed to beneficially own upon satisfaction of certain conditions. Collectively, the Physical Derivative Agreements held by the Reporting Persons represent economic exposure comparable to an interest in approximately 2.8% of the shares of Common Stock. The counterparties to the Physical Derivative Agreements are unaffiliated third party financial institutions.

Elliott, through The Liverpool Limited Partnership, a Bermuda limited partnership and a wholly-owned subsidiary of Elliott, and Elliott International have entered into notional principal amount derivative agreements in the form of cash settled swaps (the "Cash Derivative Agreements") with respect to 410,152 and 871,574 shares of Common Stock of the Issuer, respectively (representing economic exposure comparable to approximately 0.9% and 1.9% of the shares of Common Stock of the Issuer, respectively). Collectively, the Cash Derivative Agreements held by the Reporting Persons represent economic exposure comparable to an interest in approximately 2.9% of the shares of Common Stock. The Cash Derivative Agreements provide Elliott and Elliott International with economic results that are comparable to the economic results of ownership but do not provide them with the power to vote or direct the voting or dispose of or direct the disposition of the shares that are referenced in the Cash Derivative Agreements (such shares, the "Subject Shares"). The Reporting Persons disclaim beneficial ownership in the Subject Shares. The counterparties to the Cash Derivative Agreements are unaffiliated third party financial institutions.

On April 2, 2018 Elliott, Elliott International and EICA entered into a Joint Filing Agreement (the "Joint Filing Agreement") in which the parties agreed to the joint filing on behalf of each of them of statements on Schedule 13D with respect to the securities of the Issuer to the extent required by applicable law. The Joint Filing Agreement is attached as Exhibit 99.1 hereto and is incorporated herein by reference.

Except as described above in this Item 6, none of the Reporting Persons has any contracts, arrangements, understandings or relationships with respect to the securities of the Issuer. | |

| CUSIP No. 204166102 | Schedule 13D | Page 11 of 12 Pages |

| Item 7. | EXHIBITS | |

| Exhibit | Description | |

| Exhibit 99.1 - | Joint Filing Agreement | |

| Exhibit 99.2 - | Letter to the Board, dated April 2, 2018 | |

| CUSIP No. 204166102 | Schedule 13D | Page 12 of 12 Pages |

SIGNATURES

After reasonable inquiry and to the best of his or its knowledge and belief, each of the undersigned certifies that the information set forth in this statement is true, complete and correct.

DATE: April 2, 2018

| ELLIOTT ASSOCIATES, L.P. | ||

| By: Elliott Capital Advisors, L.P., as General Partner | ||

| By: Braxton Associates, Inc., as General Partner | ||

| /s/ Elliot Greenberg | ||

| Name: Elliot Greenberg | ||

| Title: Vice President |

| ELLIOTT INTERNATIONAL, L.P. | ||

| By: Elliott International Capital Advisors Inc., as Attorney-in-Fact |

||

| /s/ Elliot Greenberg | ||

| Name: Elliot Greenberg | ||

| Title: Vice President |

| ELLIOTT INTERNATIONAL CAPITAL ADVISORS INC. |

||

| /s/ Elliot Greenberg | ||

| Name: Elliot Greenberg | ||

| Title: Vice President |

SCHEDULE 1

Transactions of the Reporting Persons Effected During the Past 60 Days

The following transactions were effected directly by Elliott Associates, L.P. in the shares of Common Stock during the past 60 days:

| Date | Security | Amount of Shs. Bought / (Sold) |

Approx. price ($) per Share |

| 03/19/2018 | Common Stock | 67,859 | 57.9288 |

| 03/15/2018 | Common Stock | 27,821 | 56.6073 |

| 03/14/2018 | Common Stock | 15,847 | 55.4498 |

| 03/13/2018 | Common Stock | 75,823 | 55.5674 |

| 03/12/2018 | Common Stock | 30,005 | 54.9938 |

| 03/09/2018 | Common Stock | 24,025 | 54.7110 |

| 03/08/2018 | Common Stock | 27,373 | 53.5943 |

| 03/07/2018 | Common Stock | 21,006 | 53.1642 |

| 03/06/2018 | Common Stock | 26,234 | 52.3910 |

| 03/02/2018 | Common Stock | 36,007 | 50.7856 |

| 02/28/2018 | Common Stock | 31,212 | 52.8500 |

| 02/27/2018 | Common Stock | 22,974 | 53.0688 |

| 02/26/2018 | Common Stock | 21,385 | 53.6420 |

| 02/23/2018 | Common Stock | 6,812 | 53.2394 |

| 02/22/2018 | Common Stock | 36,934 | 52.9491 |

| 02/21/2018 | Common Stock | 29,847 | 52.8662 |

| 02/20/2018 | Common Stock | 13,699 | 52.4073 |

| 02/15/2018 | Common Stock | 1,920 | 51.9900 |

| 02/14/2018 | Common Stock | 1,116 | 51.4971 |

| 02/13/2018 | Common Stock | 20,912 | 50.9375 |

| 02/12/2018 | Common Stock | 11,200 | 50.6369 |

| 02/08/2018 | Common Stock | 24,000 | 50.8052 |

| 02/07/2018 | Common Stock | 11,222 | 51.3658 |

| 02/06/2018 | Common Stock | 6,940 | 51.2195 |

| 02/05/2018 | Common Stock | 48,000 | 51.9888 |

| 02/01/2018 | Common Stock | (3,492) | 54.0057 |

The following transactions were effected by Elliott International, L.P. in the shares of Common Stock during the past 60 days:

| Date | Security | Amount of Shs. Bought / (Sold) |

Approx. price ($) per Share |

| 03/19/2018 | Common Stock | 144,199 | 57.9288 |

| 03/15/2018 | Common Stock | 59,121 | 56.6073 |

| 03/14/2018 | Common Stock | 33,676 | 55.4498 |

| 03/13/2018 | Common Stock | 161,125 | 55.5674 |

| 03/12/2018 | Common Stock | 63,760 | 54.9938 |

| 03/09/2018 | Common Stock | 51,054 | 54.7110 |

| 03/08/2018 | Common Stock | 58,168 | 53.5943 |

| 03/07/2018 | Common Stock | 44,637 | 53.1642 |

| 03/06/2018 | Common Stock | 55,745 | 52.3910 |

| 03/02/2018 | Common Stock | 76,515 | 50.7856 |

| 02/28/2018 | Common Stock | 66,326 | 52.8500 |

| 02/27/2018 | Common Stock | 48,820 | 53.0688 |

| 02/26/2018 | Common Stock | 45,442 | 53.6420 |

| 02/23/2018 | Common Stock | 14,477 | 53.2394 |

| 02/22/2018 | Common Stock | 78,486 | 52.9491 |

| 02/21/2018 | Common Stock | 63,426 | 52.8662 |

| 02/20/2018 | Common Stock | 29,111 | 52.4073 |

| 02/15/2018 | Common Stock | 4,080 | 51.9900 |

| 02/14/2018 | Common Stock | 2,371 | 51.4971 |

| 02/13/2018 | Common Stock | 44,439 | 50.9375 |

| 02/12/2018 | Common Stock | 23,800 | 50.6369 |

| 02/08/2018 | Common Stock | 51,000 | 50.8052 |

| 02/07/2018 | Common Stock | 23,846 | 51.3658 |

| 02/06/2018 | Common Stock | 14,747 | 51.2195 |

| 02/05/2018 | Common Stock | 102,000 | 51.9888 |

| 02/01/2018 | Common Stock | (7,421) | 54.0057 |

Exhibit 99.1

JOINT FILING AGREEMENT

The undersigned hereby agree that the statement on Schedule 13D with respect to the shares of Common Stock of Commvault Systems, Inc., dated April 2, 2018, and any further amendments thereto signed by each of the undersigned shall be, filed on behalf of each of the undersigned pursuant to and in accordance with the provisions of Rule 13d-1(k) under the Securities Exchange Act of 1934, as amended.

DATE: April 2, 2018

| ELLIOTT ASSOCIATES, L.P. | ||

| By: Elliott Capital Advisors, L.P., as General Partner | ||

| By: Braxton Associates, Inc., as General Partner | ||

| /s/ Elliot Greenberg | ||

| Name: Elliot Greenberg | ||

| Title: Vice President |

| ELLIOTT INTERNATIONAL, L.P. | ||

| By: Elliott International Capital Advisors Inc., as Attorney-in-Fact |

||

| /s/ Elliot Greenberg | ||

| Name: Elliot Greenberg | ||

| Title: Vice President |

| ELLIOTT INTERNATIONAL CAPITAL ADVISORS INC. |

||

| /s/ Elliot Greenberg | ||

| Name: Elliot Greenberg | ||

| Title: Vice President |

Exhibit 99.2

Letter to the Board

Elliott

Management Corp.

40 West 57th Street

New York, New York 10019

Tel. (212)

974-6000

Fax: (212) 974-2092

April 2, 2018

The Board of Directors

Commvault Systems, Inc.

1 Commvault Way

Tinton Falls, NJ 07724

Dear Members of the Board:

We are writing to you on behalf of Elliott Associates, L.P. and Elliott International, L.P. (collectively, “Elliott” or “we”), which collectively own 10.3% of common stock and economic equivalents of Commvault Systems, Inc. (the “Company” or “Commvault”), making us one of the largest shareholders of the Company.

We are writing to you today to share our thoughts regarding the need for fundamental change at Commvault. We believe Commvault’s current value does not reflect its leadership position in the Data Management software market and that there exists a distinct and significant value opportunity at the Company. We want to make clear that we have great respect for what Bob and Al have built over the last two decades. The value creation opportunity present at Commvault today would not be possible without their leadership.

Our letter today lays out the reasons for Commvault’s share-price underperformance, outlines our proposed path forward and introduces the four highly qualified candidates we are nominating to the Commvault Board. We are releasing this letter publicly to make our views clear in conjunction with submitting our nominees for consideration at the upcoming annual meeting. We have deep experience as software investors, and our track record in technology is one of partnering with management teams and boards to find mutually supported paths to value creation. We have spent significant time and resources evaluating Commvault over several years and we hope you find our conclusions well considered.

The balance of our letter is organized as follows:

| - | About Elliott Management |

| - | Commvault’s Growth to Today |

| - | Commvault as a Public Company |

| - | The Path Forward |

| - | Next Steps |

We want to emphasize that we have done considerable work on Commvault and have great respect for what Bob and his team have built. Additionally, we have enormous appreciation for the hard-working and talented employees at Commvault who have helped build the Company into what it is today. We believe the actions proposed in this letter will result in greater innovation, enhanced go-to-market productivity, increased channel enablement and more satisfied customers. We are optimistic that we can work together with the Board to reach a collaborative agreement that will be in the best interests of the Company and its shareholders.

Elliott has a great deal of experience working constructively with companies that have faced similar issues, and we look forward to commencing our work together to create long-term, sustainable value at Commvault. Thank you for your time and for considering our thoughts.

About Elliott Management

Elliott is an investment firm founded in 1977 that today manages approximately $35 billion of capital for both institutional and individual investors. We are a multi-strategy firm based in New York, active in debt, equities, commodities, currencies and various other asset classes across a range of industries. Investing in the technology sector is one of our most active efforts at Elliott and one in which we have built a long and successful track record. Regarding Commvault, we have spent considerable time in the Company’s sector. We were recently a large shareholder of Symantec and conducted deep diligence on Veritas (among other Commvault competitors). As noted above, we have studied Commvault for several years and have a strong appreciation for and understanding of the Company’s history and challenges.

Our approach to Commvault is consistent with our approach to many of our current and previous technology investments. This diligence process encompassed extensive research to better understand the Company’s operations and strategy, including working with respected technology and management consultants to examine the broader Data Management and Backup & Recovery Software landscapes, as well as Commvault’s position within those markets. We have also evaluated the capabilities and competitive positioning of Commvault’s products and technologies across its offerings. Our efforts include a survey of IT decision-makers, enabling us to better understand the market landscape from a buyer’s perspective and to identify what factors are most important in driving purchasing behavior. We have also retained senior advisors in the enterprise software and broader technology marketplaces to advise us on higher-level corporate considerations. We believe this time- and resource-intensive exercise has given us a strong understanding of the markets in which Commvault participates, as well as a deep appreciation for the Company’s competitive strengths and challenges.

Commvault’s Growth to Today

Over the last two decades, Commvault has grown to be a leader in the Data Management industry. Over much of this time, Commvault has enjoyed strong tailwinds from the explosive proliferation of data and the importance of backing up and preserving that data. With its unified code base and leading-edge capabilities, Commvault had a successful IPO in September 2006 and subsequently enjoyed years of double-digit growth, powered by its software-centric-architecture and superior product offering. The growth and successes that helped create the Commvault of today are a credit to Bob and his executive team.

During this time, Commvault built an impressive solution set for customers, ranging from Galaxy to QiNetix to Simpana and most recently to the current Commvault branding and the re-introduction of appliances. Although widely considered a “complex” solution, participants across the industry praise Commvault for its robust feature set and high product quality. Our diligence process, which included interviews and surveys with hundreds of customers, confirmed our view that Commvault’s product quality and feature set are

unmatched in the industry. Even competitors comment that winning against Commvault is difficult unless the customer is narrowly focused on price or purchasing a bundle with storage hardware.

While we believe Commvault has the most comprehensive solution in the market, the evolution of the industry has not always gone in Commvault’s favor. Over the last five years, Commvault has been challenged by several of the most important technology trends in the market (including appliances, virtualization and hyperconverged). These trends seeded competitors that were once considered “start-ups” and are now formidable players in the market. These technology trends created opportunities for significant market-share gains that have benefited newer competitors while Commvault’s market share has not kept up over recent years. While Commvault eventually released competitive products in response, these releases were generally too late. No technology company will get 100% of market pivots correct, but Commvault’s missed opportunities have been especially material.

After evaluating Commvault with the help of our team of advisors, we see Commvault as an incredible product success story. However, having built a great platform with high-performance products is not synonymous with having a well-functioning company today. As is often the case when there are fundamental business issues, Commvault has also not been a successful investment for its shareholders. We believe Commvault’s issues are widespread, including its severe margin underperformance, suboptimal financial targets, recurring execution issues and lagging corporate governance. We believe these issues are fixable, but Commvault faces critical decisions in the immediate term.

Commvault as a Public Company

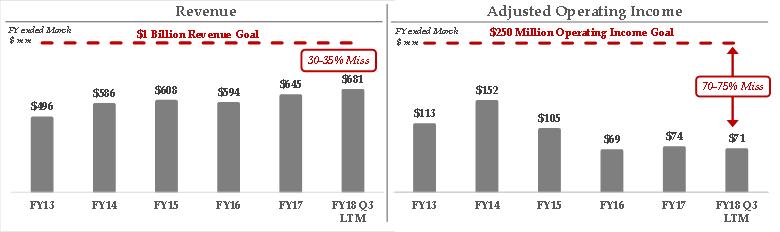

Before discussing our recommendation to the Board on a path forward, we believe it is important to outline Commvault’s situation today. Commvault has outstanding products and technology and is recognized as a market leader. Unfortunately, Commvault has not been a success story as a public-company investment, and its share-price underperformance has been profound. This underperformance stems from a lack of credibility with investors, who have lost faith due to Commvault’s recurring execution issues and its inability to drive a balanced approach to both revenue growth and margin expansion. Consider the following statistics, as described in more detail below:

| - | Since FY2013, revenue has increased by 37%, but operating income has declined by 37%; |

| - | Today, Commvault spends 77% of revenue on operating expenses (excessive relative to a broad group of relevant technology companies discussed later in the letter), which is greater than the level it spent in FY2006 when it was 1/6th the size; |

| - | Operating margins have declined by over 1,200 basis points since FY2013 despite having revenue that is nearly 40% larger (10% margin today vs. 23% margin five years ago); and |

| - | Inclusive of Commvault’s stock-based compensation, the Company has negative profitability today, which represents its lowest profitability on this basis compared to any fiscal year period since the IPO in 2006. |

We believe the cause of this underperformance is multifaceted, deriving from a confluence of issues with strategy, operations, execution, governance and capital stewardship. The reality is that Commvault is a publicly traded software company that no longer grows 20% per year. In Commvault’s new lower growth paradigm, success as a publicly traded company requires a new strategy and appropriate objectives for performance. Today, Commvault is not executing on these requirements for success, and the stock’s performance reflects this fact.

Stock-Price Performance: Commvault’s strategy, operations, execution and leadership over the past eight years have failed to generate returns to shareholders, despite a leadership position in a growing market with a product set that customers like and competitors respect. Commvault’s underperformance has been so profound that an investor would have been better off buying the NASDAQ index instead of Commvault’s stock on 99% of trading days in the last eight years[1]. The numbers speak for themselves:

Commvault’s returns have been particularly disappointing over the last five years, where recurring execution issues and a dramatic decline in operating income have weighed heavily on the stock. Even companies operating in less attractive market segments with greater secular challenges have managed to operate more efficiently, execute well and ultimately deliver shareholder value. For example, CA, NetApp, Oracle and Symantec have consistently outperformed Commvault over nearly all time periods within the last five years despite low or no revenue growth and greater industry headwinds1.

This share-price underperformance matters not only for institutional investors but also for active employees who receive part of their compensation in the form of restricted stock. Commvault, like most technology companies, provides substantial equity compensation to employees. This equity compensation is a critical component of overall compensation and is an important way to retain and recruit employee talent. Employees follow share-price performance just as closely as institutional investors. In many cases, an employee’s stock is a large portion of his or her savings. Employees pay attention when the stock is underperforming. Commvault’s prolonged underperformance drives a vicious cycle in which the inability to hire and retain key talent can drive further underperformance.

_______________

[1] Per Bloomberg. Unaffected price of February 20, 2018 represents the date prior to Elliott’s initiation of significant purchases of stock and derivatives, which represented 20% of the cumulative trading volume of Commvault’s stock after February 20 through March 29. Historical Total Return comparisons assume an investor purchases on the given historical date and holds the security through the date of the unaffected price.

Value Proposition to Investors: The underperformance discussed above is tied to Commvault’s lack of a compelling “value proposition” – i.e., the combined business and financial reasons for an investor to buy and hold shares in a given company. Until five years ago, Commvault offered a clear and appealing value proposition as an up-and-coming vendor taking market share from Veritas, IBM and EMC and growing at a revenue CAGR of more than 20% while delivering expanding operating margins. During that time, Commvault was valued for its revenue growth and earned a premium valuation from investors.

However, over the last five years, Commvault has suffered consistent execution issues, stalled revenue growth and deeply impaired profitability. The result is a value proposition to investors that is not only muddied but nearly non-existent. Since FY2013, revenue has increased by 37% while operating income has declined dramatically by 37%.

In a software market bifurcated between high-growth companies on the one hand and high-margin companies on the other, Commvault is neither. Instead, it delivers mid-range revenue growth and exceedingly low margins of just 10%. In fact, Commvault’s operating margins today rank as its lowest margins in more than a decade despite revenue growing to be more than 4x as large over the same period. After subtracting its stock-based compensation expense, Commvault is now operating at a loss, which is well below its profitability at any time since its IPO in 2006. This failure to scale margins with growing revenue stands out even compared to many software companies with similar challenges that we have encountered in the past.

Over the years, Commvault justified its accelerating operating expense investments and reduced profitability with the goal of returning to 20% software license growth. Unfortunately, Commvault is nowhere close to achieving this level of growth, and many investors question whether this goal is realistic given mid-to-high single-digit industry growth expectations. Further, Commvault significantly missed its longstanding goal of $1 billion of revenue and mid-20s operating margins within the FY2018 time period.[2]

Missing key targets like this erodes investor confidence. Setting appropriate long-term targets and then executing against those targets is essential for the Company to build trust with the investment community. When long-term financial targets remain unmet, it not only leaves investors unable to forecast the business accurately, but it also undermines investor confidence in management. The unfortunate result of these missed targets is investor distrust and unwillingness on the part of the investment community to invest behind this management team.

_______________

[2] “We are well on track in establishing the product, distribution, services, support, and marketing foundations to enable us to achieve our FY 2015 objectives, and over the next three years, to achieve our billion-dollar plan and maintain mid-20s operating margin objectives” – Commvault, January 2014.

The reason these missed targets are so detrimental to investor confidence is that they raise serious questions in investors’ minds about whether management understands the underlying trends in its business and appreciates both the competitive and customer dynamics in the industry. The implications are significant for how the Company makes budgets and forecasts. These essential operational steps drive nearly every key decision a team makes: how many sales engineers to hire, how much to invest in an R&D initiative, how to set appropriate quota levels and numerous other key decisions. An engaged Board of Directors must focus on why management’s targets are being missed so routinely, especially since the Board relies on the budget process for numerous decisions, including at the Compensation Committee level where targets are approved and incentive compensation is instituted.

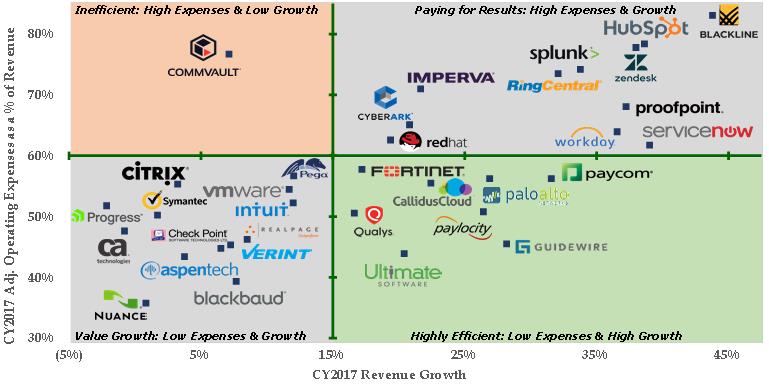

Operational Efficiency: As long-tenured directors of a public software company, you are likely familiar with the best practices for operating software companies consistent with their growth rate and opportunity set: high-growth companies can justify lower margins as they are scaling rapidly, taking market share and creating new markets. Lower-growth companies recognize their growth potential and calibrate investment levels appropriately. Commvault is not executing against this paradigm and is delivering both exceedingly low margins and low revenue growth. The chart below demonstrates just how unusual this is by comparing Commvault’s revenue growth and operating expenses to a broad group of relevant technology companies[3]:

As the chart clearly shows, Commvault’s level of inefficiency is an extreme outlier in the industry. For example, almost none of the companies in this group spend more than 75% of revenue on operating expenses, including companies that are growing more than 25% per year such as Palo Alto Networks, ServiceNow and

_______________

[3] Source: S&P Capital IQ, Street Analyst estimates, and company filings.

Commvault’s experience over the last five years has demonstrated that accelerating investment, particularly in Sales & Marketing, is not resulting in accelerating revenue growth. Instead, sales productivity has declined precipitously during this period. We believe that Commvault’s issues require a different solution. Our diligence uncovered numerous operational issues driving Commvault’s inefficiency, including complex licensing, unrealistic quota-setting, ever-changing sales coverage and high employee turnover in some functional areas. Resolution of these issues is necessary to drive not only more efficient, but vastly more effective, sales and marketing efforts.

These operational efficiency issues can be summarized through the often-cited “Rule of 40” metric for a software company where revenue growth plus operating margin at a well-run company approximates 40%. Today, Commvault is operating at approximately half that rate, one of the lowest ratios across the entire software universe.[4] This gap underscores the improvement opportunity available, which we believe is fixable in the near to medium term.

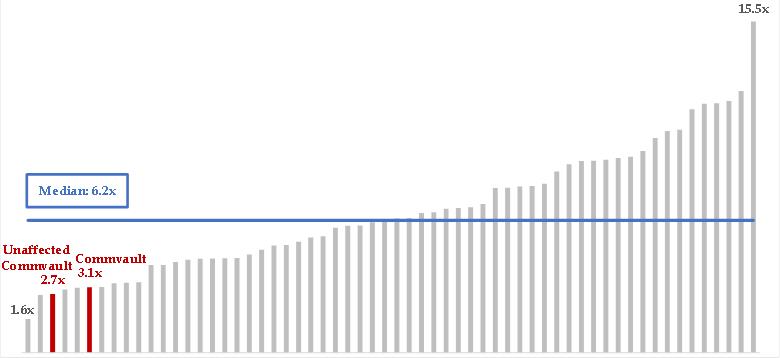

Valuation Multiples: Valuation multiples reflect many factors, including shareholder sentiment, confidence in execution, company strategy, competitive position, revenue growth prospects, earnings growth, etc. Today, we believe Commvault is deeply undervalued and that its valuation multiple does not reflect the quality of its business, position in the industry and potential long-term earnings growth. Among the 60 companies in the S&P North American Technology Software Index (IGV), Commvault, a member of this index, has the third-lowest revenue multiple[5]:

_______________

[4] Commvault ranks in the bottom ~ 5th percentile on the Rule of 40 metric in the S&P North American Technology Software Index. Excludes DVMT (due to tracking stock status), SNAP (due to dual-class, controlled status and social media industry), BB (due to hardware revenue exposure), ADSK (due to subscription transition) and DATA (due to subscription transition).

[5] Source: S&P Capital IQ and company filings. Group composed of the constituents of the S&P North American Technology Software Index. Excludes DVMT because it is a tracking stock of VMW. Commvault Unaffected multiple calculated using the unaffected price of February 20, 2018.

For context, it is important to take a closer look at the two companies with lower revenue multiples than Commvault: (1) MicroStrategy trades at 1.6x revenue, does not generate meaningful revenue growth and is a dual-class, controlled company and (2) Verint trades at 2.7x revenue and has meaningful non-software revenue with 65% gross margins. Commvault is not in good company. For the reasons highlighted in this letter, the investment community is clearly not confident in Commvault’s strategy, execution and ability to create long-term sustainable value.

Corporate Governance Issues

When operational and managerial issues have created problems for a company, there is usually an absence of appropriate governance culture and accountability as well. This is true at Commvault, where corporate governance culture at the Company has not kept up with best practices that have been widely adopted by other boards. We strongly believe that good governance is good business. Despite years of share-price underperformance, execution issues, depressed profitability and unmet targets, Commvault has experienced an absence of accountability. This reflects poorly on the Board and its commitment to fundamental oversight of the business – its primary responsibility. Consider:

| - | Nine out of 11 Directors have been on the Board for more than 10 years, including six Directors with more than 15 years of tenure. |

| - | The Lead Director has served on the Board for nearly 20 years, having originally joined as a representative of the private equity firm that once controlled Commvault but is no longer an owner of the Company. |

| - | The Board is comprised of all men, with the exception of one woman who was appointed just eight weeks ago, evidencing a lack of diversity in an area that has become an increasing focus among the largest investment institutions in their efforts to improve corporate governance. |

| - | The Company maintains a staggered Board. |

| - | Compensation at Commvault would seem to require a significant overhaul, with ISS having recommended against the Company’s “Say on Pay” proposal multiple times in recent years. |

| - | Commvault adopted a “Poison Pill” in 2008 and has never submitted this Stockholder Rights Plan to a shareholder vote. |

Despite these deficiencies, the Nomination and Governance Committee has not made sufficient efforts to align the Company’s corporate governance regime with current best practices. This neglect has real implications because of the role that corporate governance plays in dictating the “tone at the top.” Our experience indicates that lagging corporate governance standards often reflect a failure to prioritize best practices throughout the organization. Commvault should use this opportunity to upgrade its corporate-governance practices to ensure that other needed upgrades to its business practices can be implemented successfully.

The Path Forward

The share-price underperformance and operational issues highlighted in our letter clearly demonstrate that Commvault requires fundamental change. It is our strong hope that the Board agrees with this conclusion. Shareholders’ patience for the current strategy has come to an end, and we believe this view is widely shared among many stakeholders. While we reiterate our respect for what Bob and Al have accomplished over the years, we emphasize that now is the time for the Board to take significant action. Our proposal includes the following areas:

Aligning Skills and Talent to Future Challenges

Commvault’s growth to becoming an industry leader with nearly $700 million of revenue would not have been possible without management’s leadership over the last two decades. Few software companies achieve this level of scale and universal regard for their technology and solution sets. Throughout our diligence, we found that customers and competitors alike commended the Company on the quality of its solutions and its “unmatched” capabilities. Bob and his team deserve enormous credit for these achievements.

However, it is time to consider whether Commvault has the skills and experiences needed for the Company’s next phase of growth and value creation. Commvault’s performance over the last five years has stagnated, and serious execution issues have gone unaddressed. Operationally, Commvault ranks near the bottom on critical efficiency metrics, and these metrics are getting worse, not better. The necessary changes are fundamental to how Commvault does business. Minor fixes will not be sufficient. The skills and focus Commvault requires over the next five years must be profoundly different than those evidenced over the previous five.

More broadly, it is often the case that the skillset required for a company with several hundred million dollars of revenue is not the same skillset required to scale a business to $1+ billion of revenue. Scaling a go-to-market model, leveraging a two-tier channel distribution and simplifying product pricing and licensing are just a few examples of the challenges faced frequently as companies achieve Commvault’s scale.

These issues are not unique and are readily solvable. However, the organization must embrace a full change, which often requires talent in the form of executives who have seen these issues before and who bring fresh perspectives. Proven executives who have successfully performed in similar situations would add tremendous value to Commvault today.

Operational Execution

In order to begin addressing the operational issues raised throughout this letter, we believe Commvault should immediately initiate a comprehensive operational review (the “Operating Review”) led by the Board.

The Operating Review would target all areas of the business with a focus on optimization, go-to-market efficiency and laying the foundation for future profitable growth. It should be conducted by partnering with a third-party operational consulting firm. Assistance from a third party in comprehensive review situations is necessary to achieve the best results: While each situation is unique, these firms have been through similar exercises dozens of times and can draw upon their deep knowledge of industry best practices and benchmarking from numerous prior engagements. The Operating Review should be overseen by a newly formed Operating Committee of the Board, which we describe in the “Enhanced Governance and Oversight” section below.

With the help of our operational consultants and technology advisors, we have identified opportunities for improvement throughout all areas of Commvault’s operating-expense base. We believe there is significant opportunity in all functional areas of the organization for greater efficiency and reduction of non-productive spend. In fact, we believe Commvault has the ability to achieve its long-standing mid-20s operating margin target within the next three years. The cost-structure initiatives that we have identified include de-layering of management positions, re-organizing spans of control and comprehensively re-evaluating the go-to-market model. We believe these initiatives would actually create additional investment dollars in productive sales resources and expanded R&D. We look forward to sharing with you additional specifics from our detailed diligence effort.

Lastly, we want to emphasize that operational efficiency and revenue growth are not mutually exclusive, nor are innovation and execution. In fact, we have found repeatedly that eliminating inefficient and wasteful spend leads to greater focus on the initiatives that matter most and ultimately to faster revenue growth and greater innovation. We believe Commvault can become a more successful version of itself through this process, resulting in substantial benefits to customers, employees and shareholders. This belief is not based on speculation but rather has been proven in our experience time and again.

Capital Allocation

Commvault’s historical capital-allocation policies have done little to enhance shareholder value. Today, Commvault maintains a highly inefficient balance sheet with nearly $450 million of cash (earning a de minimis return), representing over 15% of the Company’s diluted equity value. Despite buying back $540 million worth of stock since the end of FY2008, Commvault’s share repurchase program has not been significant enough to offset the substantial dilution from management’s equity compensation, as the Company’s outstanding share count has actually increased during the period. One of the Company’s largest uses of cash recently was the construction of its headquarters, which coincided closely with the period when Commvault’s business experienced severe disruption. Many similar companies have gone in the opposite direction by exiting the “real estate business” and executing sale-leaseback transactions to enhance value.

Commvault is a stable company that generates positive cash flow which we believe should grow significantly over the next several years with proper operational changes. Given these factors, Commvault’s level of cash is unnecessary and highly inefficient. Commvault has never done an acquisition in its entire history other than its small equity investment in Laitek. Though we believe prudent acquisitions are a healthy part of investing for growth and technology innovation, Commvault should be focused on righting its own operations over the next year. For these reasons, Commvault can invest in its own stock by shrinking its share base immediately and setting a proper capital return program, especially given the Company’s depressed valuation and our view of potential earnings growth over the next three years.

We are advocating for a comprehensive, multi-year capital return program comprised of an accelerated share repurchase (ASR) this year and a minimum percentage of future cash flow dedicated to share repurchases thereafter. This capital program would maintain significant liquidity for an attractive acquisition opportunity (which, of course, would have to be thoroughly evaluated) and for business flexibility. Given the opportunity for value creation and the impact of these initiatives, we believe this capital return program will create meaningful value. We have specific thoughts on the amount and shape of this program and would welcome the opportunity to engage with your banker on its formation.

Enhanced Governance and Oversight

Given the long-term issues at the Company, we believe the Board would benefit from fresh perspectives, primarily in the area of operational execution, software go-to-market experience and current technology expertise. The level of required change at the Company is significant and requires a Board with new and relevant experiences to guide the Company’s turnaround. We have been involved in dozens of similar situations and have worked constructively with many companies to add top-tier, C-suite executives and experienced Board members to these companies. For Commvault, we are submitting a group of highly qualified director nominees with what we believe is the right experience to help guide the Company on its path forward.

| - | Martha Bejar: Martha is a three-time CEO and is currently the co-founder and CEO of Red Bison Advisory Group. Previously, Martha was the CEO of Unium (acquired by Nokia in March 2018), the CEO of Flow Mobile Wireless and Chair / CEO of Wipro Infocrossing Cloud Computing. Additionally, Martha serves on the Board of CenturyLink ($18B)[6] and Mitel ($1B) and was previously on the Board of Polycom ($2B). |

Martha brings strong operational skills, deep cloud computing and communications industry expertise and significant board experience from multiple public companies.

| - | Wendy Lane: Wendy is a highly accomplished Board member with deep and varied experiences across many industries. She has served on the boards of 8 public companies, including on those of Willis Towers Watson ($20B), UPM-Kymmene ($20B) (stepping down effective April 5, 2018), MSCI ($13B) and the board of Laboratory Corporation of America ($16B). She has chaired Audit, Risk and Compensation Committees and sat on Nominating, Governance & Quality and Special Committees. |

_______________

[6] Dollar amounts adjacent to Board representation companies denote market capitalization per Bloomberg.

Wendy brings significant board experience, corporate governance best practices and deep financial and M&A expertise as a former investment banker.

| - | John McCormack: John is the former CEO of Websense, a Vista Equity Partners take-private investment, which subsequently was sold to Raytheon in a highly successful transaction. Today, John is the CEO of Fidelis Cybersecurity, Executive Chairman of AppRiver and a Director of Ping Identity. |

John brings a wealth of proven operational and technology capabilities. A computer science engineer by education, John is also a proven and experienced operator. He will bring necessary operational and software best practices to Commvault.

| - | Chuck Moran: Chuck is the founder and former CEO and Chairman of Skillsoft, a leading provider of SaaS-based e-learning software, which was acquired by a private equity consortium. Chuck has deep technology experience in the software industry and has been involved in the Data Management industry for several decades. Additionally, Chuck recently joined the Board of Manhattan Associates ($3B). |

Chuck is a proven growth and operational CEO who understands how to run a growing software business. Importantly, Chuck is highly experienced in solving go-to-market challenges both as a former CEO and as a former sales leader.

We would also strongly recommend the formation of an Operating Committee of the Board tasked with overseeing the completion and execution of the Operating Review. The formation of such a committee would be the best way to ensure that the Board and Management are acutely focused on the operational turnaround while also bringing the experiences and skills of the new directors to bear on the Company’s operational challenges. We have been involved in numerous situations where an Operating Committee structure was highly effective and successful.

We look forward to engaging with the Board on these critical governance matters. The combination of the initiatives highlighted in this letter and enhanced oversight will demonstrate the Board’s commitment to enacting fundamental change.

Next Steps

Elliott strongly believes in the conclusions detailed above, and we believe that our fellow Commvault shareholders share these views. Ensuring that Commvault has the right talent for the Company’s future, bolstering the Board to provide enhanced oversight and conducting a comprehensive Operational Review would all be well received by shareholders. Elliott is confident that a value-maximizing outcome is achievable. We hope the Board finds these perspectives and observations constructive, as they are based on a significant diligence effort and guided by dozens of previous investments in companies facing similar challenges.

Now is the opportune time to undertake these actions. Waiting another several years for the same operating playbook to deliver better results will only result in continued underperformance. There is substantial work to be done to transform Commvault, and delaying these actions will subject shareholders to unnecessary and significant downside risk. We believe the following series of steps is required:

| ü | Commvault’s Board to work closely with management to best understand the skills needed to drive value and growth for the future. |

| ü | Commvault to hire a third-party consulting firm to undertake a comprehensive operational review. |

| ü | Elliott and Commvault to engage in ongoing discussions to develop a path forward, including a review of management, Board additions, specific operational goals/targets and enhancements to its corporate governance. |

| ü | Elliott to support Commvault as a long-term holder. |

We personally want to thank the Board for considering our thoughts. They were carefully developed, and we hope you see merit in them. We strongly believe that Elliott and Commvault can work together collaboratively to implement these recommendations and we are eager to sit down in person to discuss the path forward. Please let us know when we can meet to discuss next steps or if you have any questions. We look forward to a constructive dialogue and to creating significant value together at Commvault.

Best regards,

|

| |

|

Jesse Cohn Partner |

Jason Genrich Portfolio Manager |